CBOT’s ART DECO DESIGN

The CBOT building in Chicago is an artistic wonder itself. From the glistening brass front doors to John Storrs’ statue of Ceres, the Roman goddess of agriculture 45 stories above LaSalle Street, the architecture of the building is a tribute to Art Deco.

CHICAGO WHEAT FUTURES

The fifty-year wheat chart available on Barchart tracks the price of the nearby wheat contract. Prior to 1972, wheat prices were low and volatility was close to zero. The events of 1972-73 woke up the market sending prices soaring from $1.60 per bushel to over $6.00 per bushel - an almost 400% increase! The Soviet wheat deal set a new valuation for all commodities around the world – not just wheat. Since that occurred, the market has become more sensitive and responsive to events influencing price – weather, wars, politics and consumer demand. Risks are higher, rewards are higher, but the market is always right.

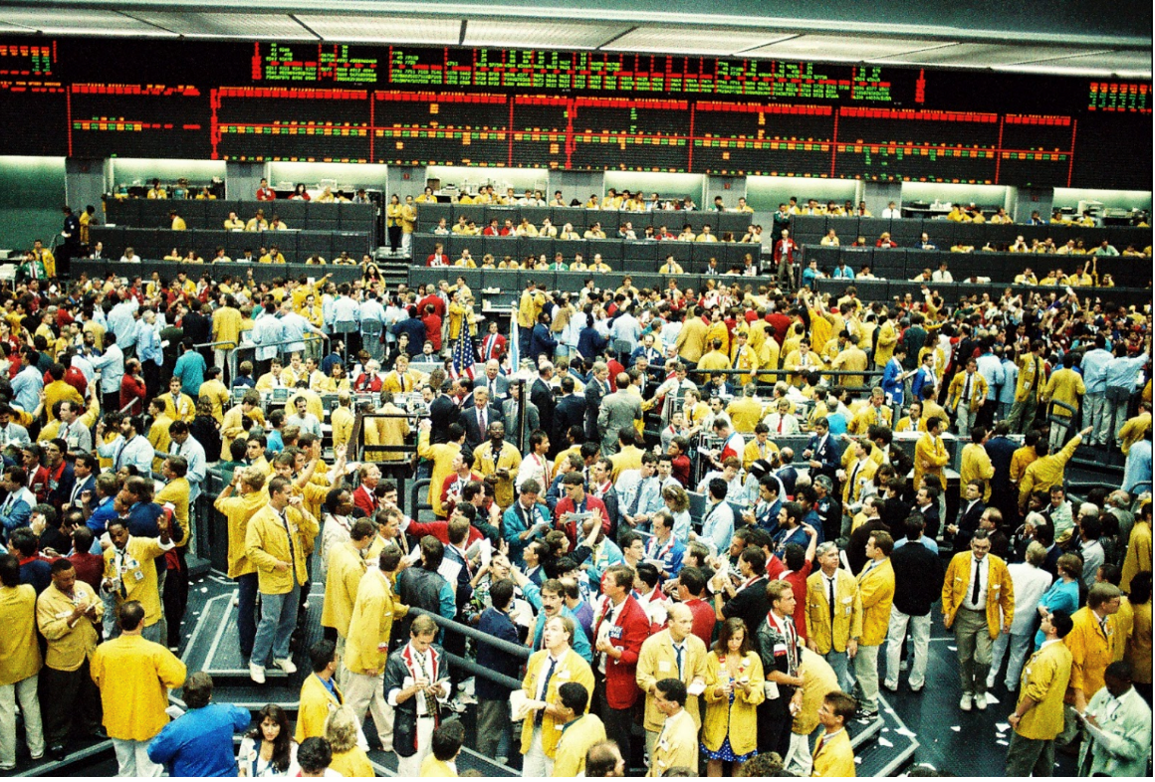

THE PIT

The steps up on the outside of the octagon and the steps down on the inside gave the pit something of the appearance of an amphitheater and allowed hundreds of traders to see and hear each other during trading hours.

Trades were made in the pits by bidding or offering a price and quantity of contracts, depending on the intention to buy (bid) or sell (offer). This is generally done by using a physical representation of a trader's intentions with his hands. If a trader wants to buy ten contracts at a price of eight, for example, in the pit he would yell "8 for 10", stating price before quantity, and turn his palm inward toward his face, putting his index finger to his forehead denoting ten; if he were to be buying one, he would place his index finger on his chin. If the trader wants to sell five contracts at a price of eight, they would yell "5 at 8", stating quantity before price, and show one hand with palm facing outward, showing 5 fingers. The combination of hand-signals and vocal representation between the way a trader expresses bids and offers is a protection against misinterpretation by other market participants.

On a typical day, in the midst of chaotic screaming and rough jockeying for position on the floor of the Chicago Board of Trade (and numerous other active trading pits around the world), no one imagined a time when this seemingly vital endeavor would be replaced by electronic impulses of ones and zeros. Trading monitors were relatively new, and the practice of live, open outcry trading sessions, unique hand signals and raucous behavior was the only accepted manner of futures market trading.

Commodity brokers and floor traders made and lost fortunes based on their ability to read the markets and react to what they saw and heard on the trading floor. This business activity required human interaction to work. There was no option. At least that’s what these denizens of the exchange believed.

There was no place like the floor of a commodity exchange anywhere else on earth.

THE EVOLUTION OF THE TRADING FLOOR

The opening bell signaled the start of trade. No deals could be consummate until the market was open. And even before the echoing ring of the opening bell subsided, it’s sound was overtaken by simultaneous yelling and arm waving of floor traders strategically positioned on the tiered levels of stairs inside the octagon stage. No trade was allowed outside the trading pit as the (human) floor monitors would not be able to capture the transactional information and relay it to the (human) board makers who skillfully transferred this data onto massive chalkboards for all to view. Simultaneously, teletype operators sent coded and abbreviated market information via ticker tape to trading houses, brokerage shops and high rolling customers all over the world.

Exuberant trade on the floor of the CBOT.

The opening bell signaled the start of trade. No deals could be consummate until the market was open. And even before the echoing ring of the opening bell subsided, it’s sound was overtaken by simultaneous yelling and arm waving of floor traders strategically positioned on the tiered levels of stairs inside the octagon stage. No trade was allowed outside the trading pit as the (human) floor monitors would not be able to capture the transactional information and relay it to the (human) board makers who skillfully transferred this data onto massive chalkboards for all to view. Simultaneously, teletype operators sent coded and abbreviated market information via ticker tape to trading houses, brokerage shops and high rolling customers all over the world.

Human activity in the cavernous space was analogous to the frantic commotion of an anthill as brokers, traders, runners and everyone else associated with the art of futures market trading scurried about their business. Phones rang, people hollered and laughter erupted spontaneously. The floor had a pulse, a rhythm defined by the swings in price and active exchange of job lots and board lots in the wheat, corn and soybean pits. Other crops like oats, soybean oil and soybean meal had their own trading pits forcing participants to vigilantly monitor those dealings as well. Futures markets had been operating for over 100 years, and everyone knew it would still be carrying on 100 years from now. At least that’s what everyone thought then.

At their pinnacle, exchanges were the most exciting and simultaneously least understood and mistrusted enterprises in any industry. Often believed to be operated and manipulated by unscrupulous traders, many participants, especially farmers, avoided any interaction with exchanges. They failed to understand the price discovery process they counted on, was based on the output of these very exchanges. Unfortunately, some of this mistrust was well founded due to the actual presence of a few market manipulators. These bad actors made all the honest traders subject to suspicion. But, over time, the exchanges cleaned up their shops, incorporated effective market surveillance and oversight and garnered the support of financial institutions. The development of clearinghouses added integrity and confidence to exchange operations. And above all, they worked. They provided effective price discovery, price transparency and a proven mechanism to transfer the risk of price change through hedging.

The modern-day equivalent of the trading floor prior to electronic trading.

The end to open outcry came quickly and silently. Exchanges announced their intention to incorporate simultaneous electronic trading along with traditional pit trading. This was represented as a technique to broaden global access, but it was really a testing ground to assess the acceptance of electronic trading as a replacement to the open outcry format. Today, no floor trading remains. It has been replaced by high speed, electronic trading platforms and instantaneous transactions. Credit concerns are a thing of the past and errors are due to fat fingers on a keyboard rather than two sellers fighting over a single buyer in the pit or an illegible entry on a trading card. Today a typical “trader” sits at a desk with multiple trading screens, executing trading algorithms and millisecond programmed trading protocols to buy and sell. My god, that sounds boring!

The art of listening to the pulse of the trade has been lost. No one can look into the eye of their counterparty to attempt to detect if they are really just selling 50 contracts or if they have 500 for sale on their order pad. The rush of a buyer and seller facing off in the pit and the odd physical altercation is gone. The drama of the opening bell and the cacophony of yelling are relics of the past but, for this story at least, we can go back to those wondrous days on the trading floor and reminisce.

Today’s young trader, raised on electronic video games and cell phone technology, probably laughs at the ancient ones and their old ways, but there are still a few of us old floor traders who remember the pit with fondness and even reverence. Those guys were the real “merchants of grain”.

Today’s commodity trading environment.